Linear Econometric Models¶

So far in our Scientific Python adventures we have covered:

NumPy

Pandas

Matplotlib

For our next adventure into Python’s Scientific stack we are going to look into estimating simple linear econometric models. This is just the tip of the iceberg as far as statistical modelling packages and capabilities in Python - but it is enough to get you hopefully confident enough to go looking for further modelling libraries on your own.

This notebook is structured a little bit like how a simple project might look. We do all the tasks needed from downloading the data, some data visualization and the econometrics together. This should show you how far we have come on our Python Adventure.

Loading some data¶

The plan is to use the data from Acemoglu, Johnson and Robinson’s 2001 AER paper (hereafter AJR) on linking institutions to economic development as an example on how to run OLS and IV style regression models. That means we have to load the data.

Importing into Pandas¶

AJR provide multiple datasets on their replication page that we have put the ‘data’ directory. Each dataset allows us to construct estimates from one of the tables in the paper.

We’ll start by working with table 1’s data, maketable1.dta.

It’s a Stata datafile, so we will need to use the function read_stata from the pandas library:

import pandas as pd

data = pd.read_stata('data/maketable1.dta')

data.head()

| shortnam | euro1900 | excolony | avexpr | logpgp95 | cons1 | cons90 | democ00a | cons00a | extmort4 | logem4 | loghjypl | baseco | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | AFG | 0.000000 | 1.0 | NaN | NaN | 1.0 | 2.0 | 1.0 | 1.0 | 93.699997 | 4.540098 | NaN | NaN |

| 1 | AGO | 8.000000 | 1.0 | 5.363636 | 7.770645 | 3.0 | 3.0 | 0.0 | 1.0 | 280.000000 | 5.634789 | -3.411248 | 1.0 |

| 2 | ARE | 0.000000 | 1.0 | 7.181818 | 9.804219 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 3 | ARG | 60.000004 | 1.0 | 6.386364 | 9.133459 | 1.0 | 6.0 | 3.0 | 3.0 | 68.900002 | 4.232656 | -0.872274 | 1.0 |

| 4 | ARM | 0.000000 | 0.0 | NaN | 7.682482 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

Data Visualization¶

AJR’s main hypothesis is to investigate the relationship between institutional differences and economic outcomes.

To do this the paper operationalizes the variables of interest as follows:

economic outcomes are proxied by log GDP per capita in 1995, adjusted for exchange rates,

logpgp95institutional differences are proxied by an index of protection against expropriation on average over 1985-95, constructed by the Political Risk Services Group,

avexpr

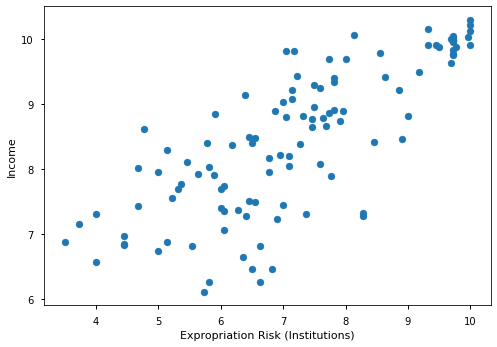

Before we jump on to running regressions, let’s check out whether there is any relationship between these variables graphically:

import matplotlib.pyplot as plt

plt.style.use('seaborn-notebook')

fig, ax = plt.subplots()

ax.scatter(data['avexpr'], data['logpgp95'])

ax.set_xlabel('Expropriation Risk (Institutions)')

ax.set_ylabel('Income')

Text(0, 0.5, 'Income')

So there definitely appears to be a positive correlation between instututions and income.

Univariate Regression¶

OK, so now we have visualized data let’s run some OLS regressions. We will start with the simplest regression we can think of to map:

To run OLS regressions we’ll need a new package, statsmodels.

First we need to load the statsmodels package:

import statsmodels as sm

sm.__version__

'0.12.2'

There’s two ways to write out the specification for a regression, the easiest is by writing a formulaic description of the regression we want to estimate:

import statsmodels.formula.api as smf

simple_reg = smf.ols('logpgp95 ~ avexpr', data=data)

To estimate the regression specification, we use the fit method:

results = simple_reg.fit()

The results object now contains a bunch of information.

Most of the ‘standard output’ we have come to expect from software like STATA are contained in the .summary():

print(results.summary())

OLS Regression Results

==============================================================================

Dep. Variable: logpgp95 R-squared: 0.611

Model: OLS Adj. R-squared: 0.608

Method: Least Squares F-statistic: 171.4

Date: Wed, 15 Sep 2021 Prob (F-statistic): 4.16e-24

Time: 12:38:13 Log-Likelihood: -119.71

No. Observations: 111 AIC: 243.4

Df Residuals: 109 BIC: 248.8

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 4.6261 0.301 15.391 0.000 4.030 5.222

avexpr 0.5319 0.041 13.093 0.000 0.451 0.612

==============================================================================

Omnibus: 9.251 Durbin-Watson: 1.689

Prob(Omnibus): 0.010 Jarque-Bera (JB): 9.170

Skew: -0.680 Prob(JB): 0.0102

Kurtosis: 3.362 Cond. No. 33.2

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

An observation was mistakenly dropped from the results in the original paper (see the note located in maketable2.do from Acemoglu’s webpage), so our coefficients differ slightly from the ones in the original paper.

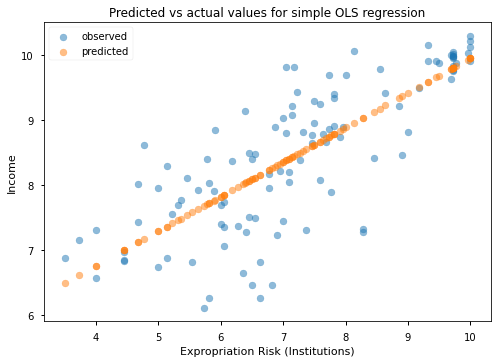

We can get the predicted values from the regression using the .predict() attribute. Let’s use these in a plot that has predicted versus actual values.

To do this, we’ll need to drop missing data from our observations because the predict() method doesn’t do well with missing data:

# Drop missing observations from whole sample

df_plot = data.dropna(subset=['logpgp95', 'avexpr'])

# Plot predicted values

fig, ax = plt.subplots()

ax.scatter(df_plot['avexpr'], df_plot['logpgp95'], alpha=0.5, label='observed')

ax.scatter(df_plot['avexpr'], results.predict(), alpha=0.5, label='predicted')

ax.set_xlabel('Expropriation Risk (Institutions)')

ax.set_ylabel('Income')

ax.set_title('Predicted vs actual values for simple OLS regression')

ax.legend()

<matplotlib.legend.Legend at 0x7f906a229a60>

We mentioned that there is two ways to call a linear regression, and so far we showed how to use the formula interface which is probably the recommended way to do this in most applications.

If we end up in a situation where we have to run a regression many times the formula interface actually slows down the code because python has to deconstruct it to get the exact information it needs. Examples where this may occur (and I have come across) are if a regression is part of a nested loop over structural parameters (BLP estimation for IO people), or if we are coding up our own indirect inference procedure.

Here’s another way to get the same result that is usually faster, although we have to import some additional functionality:

from statsmodels.tools.tools import add_constant

data = add_constant(data, has_constant='add')

/opt/hostedtoolcache/Python/3.8.11/x64/lib/python3.8/site-packages/statsmodels/tsa/tsatools.py:142: FutureWarning: In a future version of pandas all arguments of concat except for the argument 'objs' will be keyword-only

x = pd.concat(x[::order], 1)

data.columns

Index(['const', 'shortnam', 'euro1900', 'excolony', 'avexpr', 'logpgp95',

'cons1', 'cons90', 'democ00a', 'cons00a', 'extmort4', 'logem4',

'loghjypl', 'baseco'],

dtype='object')

from statsmodels.regression.linear_model import OLS

simple_reg2 = OLS(endog=data['logpgp95'],

exog=data[['const', 'avexpr']],

missing='drop')

type(simple_reg2)

statsmodels.regression.linear_model.OLS

print(simple_reg2.fit().summary())

OLS Regression Results

==============================================================================

Dep. Variable: logpgp95 R-squared: 0.611

Model: OLS Adj. R-squared: 0.608

Method: Least Squares F-statistic: 171.4

Date: Wed, 15 Sep 2021 Prob (F-statistic): 4.16e-24

Time: 12:38:13 Log-Likelihood: -119.71

No. Observations: 111 AIC: 243.4

Df Residuals: 109 BIC: 248.8

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

const 4.6261 0.301 15.391 0.000 4.030 5.222

avexpr 0.5319 0.041 13.093 0.000 0.451 0.612

==============================================================================

Omnibus: 9.251 Durbin-Watson: 1.689

Prob(Omnibus): 0.010 Jarque-Bera (JB): 9.170

Skew: -0.680 Prob(JB): 0.0102

Kurtosis: 3.362 Cond. No. 33.2

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Notice that this gives us exactly the same results.

Multivariate Regression¶

Univariate regression is rarely enough in social science. At a bare minimum we are worried about other factors affecting GDP that are not included in our model that are also correlated with institutional quality. As reasonably good econometricians we know that this causes bias / inconsistency in our estimates for \(\hat{\beta}\).

So let’s add more regressors! AJR argue that climate influences economic outcomes, and it is probably correlated to institutional quality (Discuss / think about why). They operationalize this by including latitude as a proxy.

Notice that our current data, data, doesn’t have that variable due to the ‘interesting’ way Acemoglu structures his data and do files on the web. We’ll need the data maketable2.dta:

# import new data by overwriting the old one

data = pd.read_stata('data/maketable2.dta')

Now, using the formula interface we can readily add this variable:

reg2 = smf.ols('logpgp95 ~ avexpr + lat_abst', data=data)

results2 = reg2.fit()

print(results2.summary())

OLS Regression Results

==============================================================================

Dep. Variable: logpgp95 R-squared: 0.623

Model: OLS Adj. R-squared: 0.616

Method: Least Squares F-statistic: 89.05

Date: Wed, 15 Sep 2021 Prob (F-statistic): 1.42e-23

Time: 12:38:13 Log-Likelihood: -118.09

No. Observations: 111 AIC: 242.2

Df Residuals: 108 BIC: 250.3

Df Model: 2

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 4.8729 0.328 14.855 0.000 4.223 5.523

avexpr 0.4635 0.055 8.352 0.000 0.353 0.573

lat_abst 0.8722 0.488 1.788 0.077 -0.094 1.839

==============================================================================

Omnibus: 6.082 Durbin-Watson: 1.756

Prob(Omnibus): 0.048 Jarque-Bera (JB): 5.950

Skew: -0.567 Prob(JB): 0.0510

Kurtosis: 3.037 Cond. No. 57.4

==============================================================================

Notes:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

This is nice - but its a little hard to compare coefficients and the like across regressions that are far apart in the notebook. What we really want is a regression table that summarizes all of our results. statsmodels allows us to do this too:

from statsmodels.iolib.summary2 import summary_col

info_dict={'R-squared' : lambda x: "{:.2f}".format(x.rsquared),

'No. observations' : lambda x: "{0:d}".format(int(x.nobs))}

results_table = summary_col(results=[results,results2],

float_format='%0.2f',

stars = True,

model_names=['Model 1',

'Model 2'],

info_dict=info_dict,

regressor_order=['avexpr',

'lat_abst',

'const'])

results_table.add_title('Table - OLS Regressions')

print(results_table)

Table - OLS Regressions

================================

Model 1 Model 2

--------------------------------

avexpr 0.53*** 0.46***

(0.04) (0.06)

lat_abst 0.87*

(0.49)

Intercept 4.63*** 4.87***

(0.30) (0.33)

R-squared 0.61 0.62

R-squared Adj. 0.61 0.62

R-squared 0.61 0.62

No. observations 111 111

================================

Standard errors in parentheses.

* p<.1, ** p<.05, ***p<.01

If we decide we want this table as latex output we can do that too:

with open('ols_summary.tex', 'w') as file_handle:

file_handle.write(results_table.as_latex())

Notice we did not provide a file path, so the results are saved to our current working directory.

Challenge¶

It’s your turn!

Add the following variables to the regression using the formula interface:

‘asia’, ‘africa’, ‘other’

Add the same variables as (1); but use the alternative interface that requires you to specify ‘endog’ and ‘exog’ variables

Export the results to a latex file ‘out/tables/ols-regressions’. Give the columns meaningful names, and make sure you don’t have stars in your output to satisfy the new AER policy.

Robustifying Standard Errors¶

So far our regressions have imposed heteroskedastic standard errors.

A simple test for Heteroskedasticity is the Breusch Pagan test:

reg3 = smf.ols('logpgp95 ~ avexpr + lat_abst + asia + africa + other', data=data)

results3 = reg3.fit()

from statsmodels.compat import lzip

import statsmodels.stats.api as sms

name = ['Lagrange multiplier statistic', 'p-value',

'f-value', 'f p-value']

test = sms.het_breushpagan(results3.resid, results3.model.exog)

lzip(name, test)

---------------------------------------------------------------------------

AttributeError Traceback (most recent call last)

/tmp/ipykernel_2403/307859961.py in <module>

1 name = ['Lagrange multiplier statistic', 'p-value',

2 'f-value', 'f p-value']

----> 3 test = sms.het_breushpagan(results3.resid, results3.model.exog)

4 lzip(name, test)

AttributeError: module 'statsmodels.stats.api' has no attribute 'het_breushpagan'

There is some evidence for heteroskedasticity. Let’s robustify standard errors. Statsmodels has ‘HC0’ ‘HC1’, ‘HC2’ and ‘HC3’ standard errors. The STATA default is HC1, so for better or worse let’s get a summary with those:

robust_ols = reg3.fit(cov_type='HC1')

print(robust_ols.summary())

OLS Regression Results

==============================================================================

Dep. Variable: logpgp95 R-squared: 0.715

Model: OLS Adj. R-squared: 0.702

Method: Least Squares F-statistic: 97.09

Date: Thu, 17 Aug 2017 Prob (F-statistic): 9.39e-38

Time: 17:09:20 Log-Likelihood: -102.45

No. Observations: 111 AIC: 216.9

Df Residuals: 105 BIC: 233.2

Df Model: 5

Covariance Type: HC1

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 5.8511 0.293 19.936 0.000 5.276 6.426

avexpr 0.3896 0.051 7.638 0.000 0.290 0.490

lat_abst 0.3326 0.442 0.752 0.452 -0.535 1.200

asia -0.1531 0.181 -0.848 0.396 -0.507 0.201

africa -0.9164 0.154 -5.946 0.000 -1.218 -0.614

other 0.3035 0.174 1.741 0.082 -0.038 0.645

==============================================================================

Omnibus: 4.342 Durbin-Watson: 1.865

Prob(Omnibus): 0.114 Jarque-Bera (JB): 3.936

Skew: -0.457 Prob(JB): 0.140

Kurtosis: 3.126 Cond. No. 58.2

==============================================================================

Warnings:

[1] Standard Errors are heteroscedasticity robust (HC1)

There are also options for clustered standard errors. A nice summary of what is available albiet on a different data set is available here

Instrumental Variables Estimation¶

AJR discuss that the OLS regression results may suffer from endogeneity due to:

richer countries may be able to afford or prefer better institutions

variables that affect income may also be correlated with institutional differences

the construction of the index may be biased; analysts may be biased towards seeing countries with higher income having better institutions

They propose a 2SLS solution using settler mortality to instrument for institutional differences: They hypothesize that higher mortality rates of colonizers led to the establishment of institutions that were more extractive in nature (less protection against expropriation), and these institutions still persist today.

Data for the IV regressions are contained in the file maketable4.dta from AJR’s replication files. So we will start by loading that:

data = pd.read_stata('data/maketable4.dta')

data.head()

| shortnam | africa | lat_abst | rich4 | avexpr | logpgp95 | logem4 | asia | loghjypl | baseco | |

|---|---|---|---|---|---|---|---|---|---|---|

| 0 | AFG | 0.0 | 0.366667 | 0.0 | NaN | NaN | 4.540098 | 1.0 | NaN | NaN |

| 1 | AGO | 1.0 | 0.136667 | 0.0 | 5.363636 | 7.770645 | 5.634789 | 0.0 | -3.411248 | 1.0 |

| 2 | ARE | 0.0 | 0.266667 | 0.0 | 7.181818 | 9.804219 | NaN | 1.0 | NaN | NaN |

| 3 | ARG | 0.0 | 0.377778 | 0.0 | 6.386364 | 9.133459 | 4.232656 | 0.0 | -0.872274 | 1.0 |

| 4 | ARM | 0.0 | 0.444444 | 0.0 | NaN | 7.682482 | NaN | 1.0 | NaN | NaN |

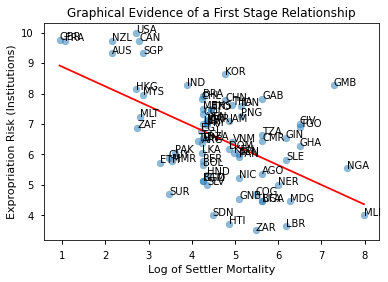

A scatter plot provides some evidence towards the necessary condition of a correlation between the instrument and the endogenous variable.

# add numpy so we can get a linear prediction to add to plot

import numpy as np

# Dropping NA's is required to use numpy's polyfit

df_plot = data.dropna(subset=['logem4', 'avexpr'])

labels = df_plot['shortnam']

fig, ax = plt.subplots()

ax.scatter(df_plot['logem4'], df_plot['avexpr'], alpha=0.5)

# add a linear prediction line on the fly

ax.plot(np.unique(df_plot['logem4']),

np.poly1d(np.polyfit(df_plot['logem4'], df_plot['avexpr'], 1))(np.unique(df_plot['logem4'])),

color='red')

# add labels to points

for i, label in enumerate(labels):

plt.annotate(label, (df_plot['logem4'].iloc[i], df_plot['avexpr'].iloc[i]))

ax.set_xlabel('Log of Settler Mortality')

ax.set_ylabel('Expropriation Risk (Institutions)')

ax.set_title('Graphical Evidence of a First Stage Relationship')

Text(0.5, 1.0, 'Graphical Evidence of a First Stage Relationship')

Let’s estimate the first stage relationship for the univariate regression model.

To do this and get results similar to AJR we will need to work on a subset of the data where baseco == 1, essentially where there are complete data on observations.

data = data.query('baseco ==1')

first_state_reg = smf.ols('avexpr ~ logem4',

data=data)

print(first_state_reg.fit(cov_type='HC1').summary())

OLS Regression Results

==============================================================================

Dep. Variable: avexpr R-squared: 0.270

Model: OLS Adj. R-squared: 0.258

Method: Least Squares F-statistic: 16.32

Date: Mon, 13 Sep 2021 Prob (F-statistic): 0.000150

Time: 12:26:10 Log-Likelihood: -104.83

No. Observations: 64 AIC: 213.7

Df Residuals: 62 BIC: 218.0

Df Model: 1

Covariance Type: HC1

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 9.3414 0.704 13.264 0.000 7.961 10.722

logem4 -0.6068 0.150 -4.040 0.000 -0.901 -0.312

==============================================================================

Omnibus: 0.035 Durbin-Watson: 2.003

Prob(Omnibus): 0.983 Jarque-Bera (JB): 0.172

Skew: 0.045 Prob(JB): 0.918

Kurtosis: 2.763 Cond. No. 19.4

==============================================================================

Notes:

[1] Standard Errors are heteroscedasticity robust (HC1)

So the first stage seems OK with a t-state > 3 (approx F > 10).

Let’s do an IV2SLS estimation.

statsmodels does not have the functionality to do IV regression, so we’ll need a new package – linearmodels.

We’ll only borrow the IV2SLS function from the iv module:

from linearmodels.iv import IV2SLS

iv_regression = IV2SLS.from_formula('logpgp95 ~ 1 + [avexpr ~ logem4]',

data=data).fit()

/home/lachlan/anaconda3/lib/python3.7/site-packages/linearmodels/iv/data.py:25: FutureWarning: is_categorical is deprecated and will be removed in a future version. Use is_categorical_dtype instead

if is_categorical(s):

Somewhat differently from statsmodels, the summary which prints out the STATA-esque regression output is an attribute of the fitted model:

iv_regression.summary

| Dep. Variable: | logpgp95 | R-squared: | 0.1870 |

|---|---|---|---|

| Estimator: | IV-2SLS | Adj. R-squared: | 0.1739 |

| No. Observations: | 64 | F-statistic: | 28.754 |

| Date: | Mon, Sep 13 2021 | P-value (F-stat) | 0.0000 |

| Time: | 12:26:20 | Distribution: | chi2(1) |

| Cov. Estimator: | robust | ||

| Parameter | Std. Err. | T-stat | P-value | Lower CI | Upper CI | |

|---|---|---|---|---|---|---|

| Intercept | 1.9097 | 1.1740 | 1.6267 | 0.1038 | -0.3912 | 4.2106 |

| avexpr | 0.9443 | 0.1761 | 5.3623 | 0.0000 | 0.5991 | 1.2894 |

Endogenous: avexpr

Instruments: logem4

Robust Covariance (Heteroskedastic)

Debiased: False

Unfortunately there is no way to currently get the outputs from a regression estimated via linearmodels into a regression table!

Final Challenge¶

Estimate the IV model for the regression that includes ‘asia’, ‘africa’ and ‘other’ as exogenous explanatory variables

Use a robust Hausman test to conduct a formal test for endogeneity. Was the IV strategy appropriate based on this test result?